It is estimated that about 75% of the global population lives in middle-income countries.

Image source:Unsplash

Spencer Feingold

Digital Editor, World Economic Forum

The "middle-income trap" refers to the situation where middle-income economies struggle for an extended period to transition into high-income economies.

According to World Bank statistics, 108 countries are currently trapped in the "middle-income trap."

World Bank Chief Economist Indermit Gill revealed to the World Economic Forum, "Most middle-income countries are still stuck with last century's approach to economic development."

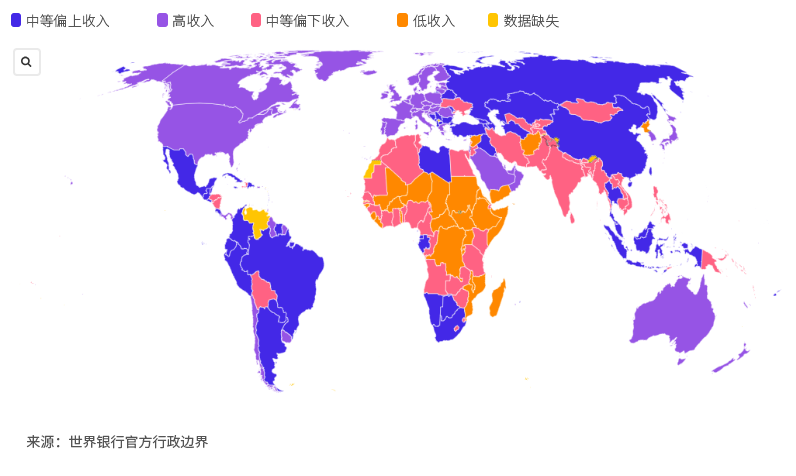

In 2007, a World Bank report introduced the concept of the "middle-income trap." At the time, the term was primarily used to describe countries in Latin America and the Middle East, which, despite economic growth and declining poverty rates, consistently struggled to transition into high-income nations.Today, according to the World Bank's "2024 World Development Report," the "middle-income trap" continues to challenge more than 100 countries worldwide. But what exactly is the "middle-income trap"?More importantly, how can the country overcome it—or even completely avoid this trap altogether?Economic Efficiency MetricsAt the end of 2023, the World Bank defined middle-income countries as economies with a per capita Gross National Income (GNI) ranging from $1,136 to $13,845. Within this group, countries are further categorized into lower-middle-income nations (GNI between $1,136 and $4,465) and upper-middle-income nations (GNI from $4,466 to $13,845).According to a World Bank report, about 75% of the global population currently lives in middle-income countries, with roughly 66% of them living in extreme poverty. The report also highlights that middle-income nations account for 40% of the world’s economic output.Image source:The World Economic Forum produced by Flourish

The World Bank says that currently 108 countries—including major economies like China, Brazil, Turkey, and India—are stuck in the "middle-income trap."

The World Bank report describes the "middle-income trap" as a formidable challenge faced by middle-income countries in terms of economic growth, wage competitiveness, and innovation—challenges that often leave these nations overly reliant on "policies anchored in measures designed to demonstrate economic efficiency." The report also highlights that this situation makes middle-income countries "particularly vulnerable to prematurely slowing their development momentum."In a separate report, the International Monetary Fund noted that countries that have fallen into the "middle-income trap" in recent decades find themselves "caught between the rapidly advancing technologies of affluent nations and the competition from mature products of low-wage, impoverished economies."The World Bank believes that the growth prospects of middle-income countries depend on their ability to innovate and boost productivity—something that remains challenging for many economies to achieve at scale. The report also notes that, if current growth rates persist, many middle-income nations may need generations of effort before they can attain high-income status.Indemitt Gill, Chief Economist of the World Bank and the World Economic Forum, told the forum: "Most middle-income countries are still relying on 20th-century approaches to economic development, focusing their policies primarily on attracting investment. It’s like driving a car stuck in first gear—no matter how hard you press the accelerator, it’ll take forever to reach your destination."In recent decades, only a few dozen countries have transitioned from middle-income status to high-income status, including Saudi Arabia, Latvia, Bulgaria, and South Korea, among others.In its report, the World Bank outlines a three-pronged approach to help countries escape the "middle-income trap." This strategy, dubbed the "3i Strategy," involves strategically adjusting economic policies related to investment, the infusion of technological resources, and innovation.First, low-income countries should focus primarily on boosting investment in their economies. For instance, in 2001, Colombia implemented a series of reforms—such as capping government spending, adopting a floating exchange rate, and strengthening the central bank’s independence—that helped increase domestic investment.Once a country enters the lower-middle-income bracket, it should adjust its policies to promote a combination of investment and technology infusion. In particular, the focus of this infusion should be on expanding the adoption of advanced technologies.After reaching upper-middle-income levels, countries should complement investment and inject momentum through innovation. The report notes that boosting innovation requires "reshaping the structures of businesses, jobs, and energy use, while placing greater emphasis on economic freedom, social mobility, and political competitiveness."The World Bank report praised South Korea as a model country for effectively implementing the 3i strategy.In the 1970s and 1980s, South Korea implemented reforms that encouraged private investment and introduced industrial policies aimed at enhancing technological adoption and boosting productivity. The resulting economic growth was nothing short of remarkable—according to World Bank data, South Korea’s per capita income soared from $1,200 in 1960 to $33,000 by 2023.Gil added that, to achieve high-income status, governments of middle-income countries "must implement competition policies and foster a healthy balance," ensuring balanced growth for companies ranging from large corporations to startups.Gil said, "When decision-makers stop fixating on company size and instead focus more on the value companies bring to the economy, and when they encourage all citizens to move up the economic ladder rather than clinging to zero-sum policies aimed at reducing income inequality, the benefits will be maximized."Experts point out that achieving sustainable economic development in low- and middle-income countries is no easy task, especially given the ongoing economic uncertainties that continue to weigh heavily on the global economy.Gil said, "Today's middle-income countries are facing heavier burdens than their counterparts have ever experienced before: aging populations, geopolitical and trade tensions, as well as the growing need to accelerate growth without harming the environment."Nevertheless, the World Bank has outlined new strategies to boost economic growth in its "2024 World Development Report," aiming to make the notion of the "middle-income trap" entirely obsolete.

The above content represents the author's personal views only.This article is translated from the World Economic Forum's Agenda blog; the Chinese version is for reference purposes only.Feel free to share this in your WeChat Moments; please leave a comment below if you'd like to republish.

Translated by: Sun Qian | Edited by: Wang Can

The World Economic Forum is an independent and neutral platform dedicated to bringing together diverse perspectives to discuss critical global, regional, and industry-specific issues.

Follow us on Weibo, WeChat Video Accounts, Douyin, and Xiaohongshu!

"World Economic Forum"