- To read the report, please click "Read More."

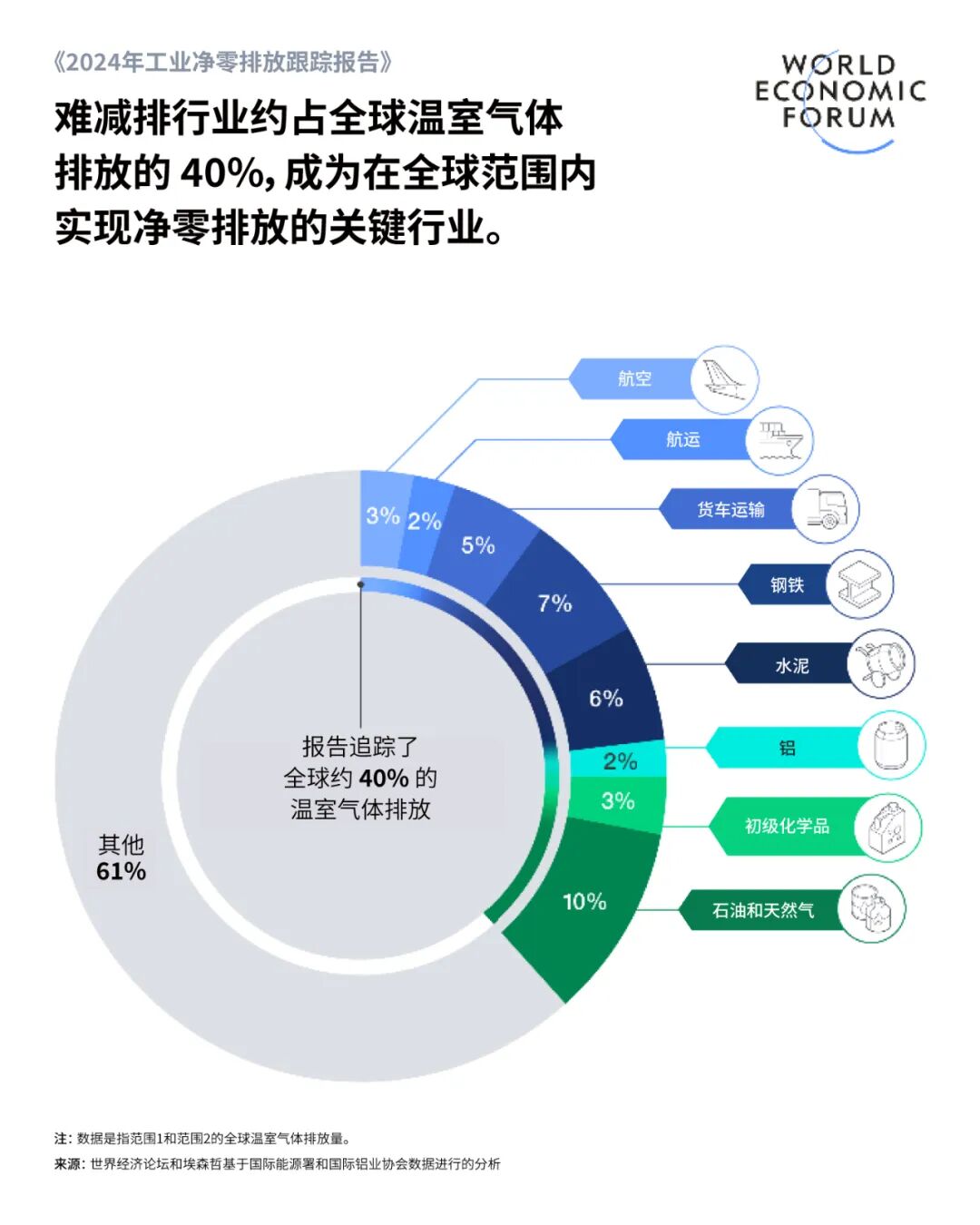

The World Economic Forum's newly released "Net-Zero Industry Tracker" report reveals that eight hard-to-abate sectors—steel, aluminum, cement, basic chemicals, oil and gas, aviation, shipping, and freight transport—have made progress in reducing their emissions. These eight critical industries are vital to the global economy, managing to cut their absolute emissions by 0.9% between 2022 and 2023, even as global energy-related emissions rose by 1.3% during the same period.However, at the current pace of progress, we are still far from achieving our net-zero emissions target. The report reveals that to reach net-zero by 2050, an additional $30 trillion in investment will be required—clearly underscoring just how daunting the challenges ahead are. To meet this massive investment demand, the eight key industries mentioned above will need to commit $13 trillion directly, while the broader ecosystem—including their energy suppliers—will have to contribute an additional $17 trillion.The recently released research report also reveals encouraging news: commercially viable technologies are already in place, capable of supporting nearly half of the global greenhouse gas reduction targets. The report further highlights that emission intensity—the average emissions per unit of output—has dropped by 4.1% over the past five years, underscoring the effectiveness of current solutions being implemented. To move forward and unlock the transformative potential of emerging technologies, it’s crucial to strengthen collaboration across industries, accelerate the deployment of clean energy infrastructure—particularly renewable power facilities—and simultaneously make more robust policy decisions.The "2024 Industrial Net-Zero Emissions Tracking Report," jointly prepared by the World Economic Forum and Accenture, assesses the current state and future trends of energy transitions across eight hard-to-abate industries—responsible for roughly 40% of global greenhouse gas emissions. It also identifies key barriers to achieving net-zero targets and outlines actionable pathways to accelerate progress, including the development of a comprehensive "readiness framework" focused on relevant technologies, investment strategies, and policy measures."While the path to emissions reduction is long, we’re encouraged by the fact that even industries traditionally hardest to decarbonize are making tangible progress—proof that they’re actively driving the energy transition," said Roberto Bocca, Managing Director of the World Economic Forum’s Centre on Energy and Materials. "To achieve net-zero emissions by 2050, every sector will need to collaborate on an unprecedented scale and unleash groundbreaking financial innovation to mobilize the capital required for these ambitious efforts. In reality, we already have many of the technologies and policy frameworks in place—so now is the time to act."

In 2022-2023, while the eight major industries increased their output, they still managed to reduce overall emissions by 0.9%. Given the global rise in emissions during the same period, these eight industries have made significant progress. More importantly, from 2019 to 2023, despite an average annual demand growth of 9.2% across these hard-to-abate sectors, both total emissions and emission intensity actually declined—demonstrating that reductions were driven not by production cuts, but rather by improved efficiency and accelerated decarbonization efforts. Among these eight challenging industries, aluminum, cement, chemicals, aviation, and heavy-duty trucking saw a notable decrease in energy intensity, thanks to a combination of factors: higher adoption of low-carbon electricity, reduced coal consumption, enhanced energy efficiency, and greater use of recycled metals.The report highlights the key challenges these industries face in their efforts to reduce emissions, including high interest rates, political uncertainty, trade restrictions, and limited options for emerging clean energy technologies. Significant investment is needed, with a particular focus on building low-carbon power systems, hydrogen infrastructure, and facilities for carbon capture, utilization, and storage. While progress has been positive in developing low-carbon power infrastructure, hydrogen and carbon capture, utilization, and storage systems currently account for less than 1% of the industry’s overall requirements.This year's report for the first time highlights the potential of generative AI in accelerating decarbonization efforts across hard-to-abate industries. By boosting productivity, streamlining operational processes, and optimizing energy use, generative AI is expected to enhance capital efficiency by 5–7% while reducing net-zero investment needs by as much as $2 trillion. Beyond cost savings, AI can also enable carbon reporting at the product level, providing powerful tools for asset management, speeding up R&D timelines, and increasing transparency in innovation processes. However, widespread adoption of AI could significantly ramp up electricity demand, raising concerns about competition for limited, low-carbon energy resources."Heavy industry is key to achieving global decarbonization goals, and artificial intelligence demonstrates real potential in helping tackle the net-zero challenge," said Muqsit Ashraf, CEO of Accenture Strategy. "Leaders who harness the productivity gains and economic value offered by generative AI are already paving the way for a transformative approach to business growth—enabling not only the avoidance of additional emissions but also unlocking AI's full promise, positioning it as a critical driver for decarbonizing entire industries."Espen Mehlum, Global Head of Energy Transformation Insights at the World Economic Forum, added: "Hard-to-abate industries must adopt systemic strategies to simultaneously address the multiple challenges tied to scaling clean energy technologies and building critical infrastructure. Policymakers can accelerate decarbonization efforts—and ultimately benefit everyone—by implementing targeted incentives aligned with the goals of hard-to-abate sectors, energy suppliers, and consumers alike."

Changes in the "2024 Industrial Net-Zero Emissions Tracking Report"

Previous versions of the report identified synthetic ammonia as one of the eight hardest-to-abate industries, but this year’s report broadened the scope to include a range of primary chemicals—ethylene, propylene, benzene, toluene, mixed xylene, ammonia, and methanol—bringing these sectors into the same category. Together, these chemicals account for 2.5% of global greenhouse gas emissions. This shift significantly increases the total emissions tracked by the report.

The World Economic Forum is an independent and neutral platform dedicated to bringing together diverse perspectives to discuss critical global, regional, and industry-specific issues.

Follow us on Weibo, WeChat Video Accounts, Douyin, and Xiaohongshu!

"World Economic Forum"